Rates move, but your plan can adapt. Use this guide to understand how mortgage rates affect your monthly payment, purchasing power, and loan options. Then, explore strategies—rate locks, buydowns, and incentives—that help you purchase with confidence in Daybreak.

Why rates matter

Small changes add up. A one‑percentage‑point shift can noticeably change your monthly payment and total interest over time. Therefore, smart timing and the right loan structure can keep your budget balanced while you choose a home and village that fit.

What moves rates

- Inflation & economic reports: Markets react to CPI, jobs data, and growth metrics.

- Fed policy expectations: Mortgage rates track the bond market, which responds to the Fed’s signals.

- Investor demand: Appetite for mortgage‑backed securities can nudge rates up or down.

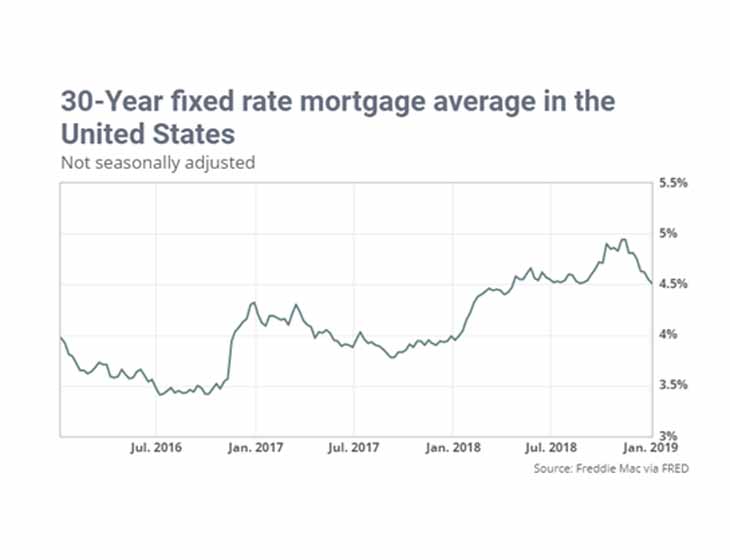

Pro tip: For historical context and weekly trend commentary, check the Freddie Mac PMMS and consumer guidance from the CFPB Explore Rates.

Buyer strategies (lock, buydown, points)

Rate lock

Lock early to protect your approval from short‑term market swings. Alternatively, ask about float‑down options if rates drop before closing.

Temporary buydown

Consider a 2‑1 or 1‑0 buydown that lowers your payment for the first years—sometimes paired with builder incentives.

Discount points

Paying points can reduce your rate for the life of the loan. However, run the break‑even math based on how long you plan to own.

Common loan programs

- Conventional: Flexible terms for strong credit profiles.

- FHA: Lower down‑payment minimums; review FHA basics from HUD.

- VA: Powerful no‑down‑payment benefits for eligible veterans; see the VA Home Loan program.

- Utah Housing Corporation: Explore down‑payment assistance options with UHC.

Run the numbers

Next, translate rates into a monthly payment. Use your lender’s calculator or the CFPB’s tools to compare scenarios—then bring those results to your model‑home tours.

Next steps in Daybreak

- Tour homes: Start at the Information Center, then see model homes and move‑in ready homes.

- Compare villages: Explore villages & districts to match your lifestyle and budget.

- Ask about incentives: Builders may offer closing‑cost credits or buydowns on select homes.

Helpful links

- Original post: Mortgage Rates

- Freddie Mac PMMS (weekly rates)

- CFPB: Explore Rates · Loan Estimate tool

- Utah Housing Corporation · VA Home Loan Types

*We love sharing tips, but this isn't a substitute for expert guidance. Always connect with a qualified real-estate pro for personalized advice.